Economic Performance & Outlook

Since the crash of 2008, markets have craved a return to the conventional economic cycle of the post second world war era. A cycle of around five years provided a period of super growth followed by a slowdown, with governments (or central banks) attempting to dampen the extremes. 2017/2018 saw optimism building for a reversion to this pattern for much of the developed world. A return of ‘normal’ growth allowed central banks to consider raising interest rates to slow down overheating economies. Indeed, the US had clearly entered this phase – with some dispute between the President and the Fed as to when to apply the brakes.

In autumn 2019, the picture looks very different, most markedly with interest rates. After rising through 2018, rates now sit as low as ever. German rates are negative through most durations; Japan is not much better. In the US, yields have dropped by nearly two per cent across the curve. Not surprisingly, this has spooked investors: it seems intuitively wrong to pay to lend to someone for 30 years. The knock-on effects must be major, whether in attitudes to saving or the workings of banks.

So is there something very odd about the state of the world economy? There are all sorts of worrying features, especially on trade, but it is hard to argue that these are exceptional, nor have they done much damage thus far. What is odd is that years of easy monetary policy and economic growth has failed to produce inflation – despite firm labour markets. While a world awash with cash has driven asset prices ever higher, consumer prices have failed to follow suit.

Cheaper money has also supported 2019’s stockmarket growth, particularly given weak global growth forecasts. We expect higher volatility in the period ahead.

A sustained period of higher asset prices is likely to cause serious side effects. Two examples of this are inflated house prices and wealth inequalities between those who have assets – generally older people – and those who do not. It is surprising that there has not been more discussion of the negative side effects of long-term quantitative easing. So far, all the talk has been of the dangers of stopping too early – more thought on the risks of entering a second decade of moribund interest rates would be constructive.

We remain long-term investors and must look beyond the immediate to the longer term. On balance, we think that increasing risk and a slowdown in the US economy will start to loom larger as we move into 2020.

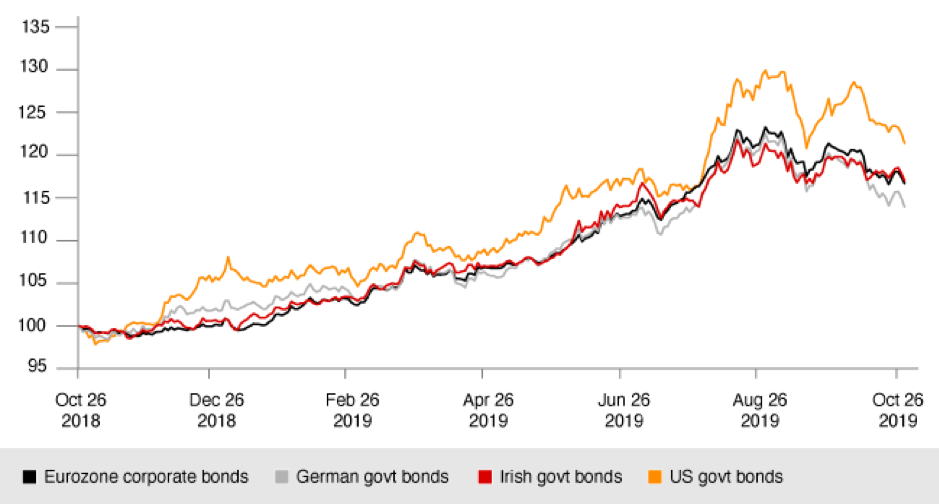

Bonds

Bond performance over past year

All bonds 10+ years, 26/10/2018 – 26/10/2019, local pricing

German 10-year bond yields have remained in negative territory through most of 2019 amid growing concern about the outlook for the euro zone’s largest economy. Expansion in credit margins offers some very limited scope, particularly in shorter-term stocks. There appear to be some opportunities in emerging market debt, whose yields have moved less than other forms of debt.

We believe that bond duration should be kept short as longer yields fail to compensate for extra risk.

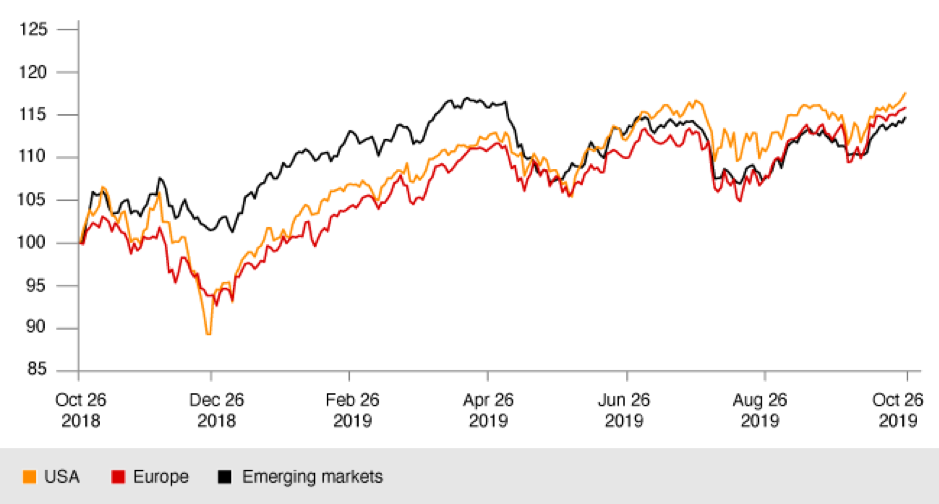

Equities

Equity performance over past year

29/10/2018 – 29/10/2019, local pricing

In recent years the US stockmarket has generally been an outperformer, driven in large part by growing tech stocks. Through 2019, this has been much less pronounced, and we believe we may well be seeing a swing away from growth stocks after years of outperformance. A similar argument may be applied to emerging market equities which have under-performed over the medium term. While rising risk has been an issue here, there does seem to be a case for looking at stocks and markets which have been out of favour in the last five years.

We are also seeing an increasing recognition that a long period of very low interest rates has consequences for bodies which depend on asset returns for their prosperity. The obvious examples here are banks, life insurance companies and pension funds. The longer that central banks keep interest rates low, the worse this will get.

Overall, valuations are looking stretched in absolute terms, although cheap relative to bonds.

European Property

Property prices have recovered sufficiently in many countries to allow profitable new developments. Property yields are still attractive relative to other asset classes, despite illiquidity.

We continue to believe that property exposure is sensible, and the long-term outlook for European property appears sound, as markets recover from a period of rental weakness. The Irish commercial market, where some of our clients’ money is, looks slightly expensive and we are recommending clients to start to disinvest in favour of more diversified European holdings but we recognise that some clients may prefer to retain their property exposure in this market.

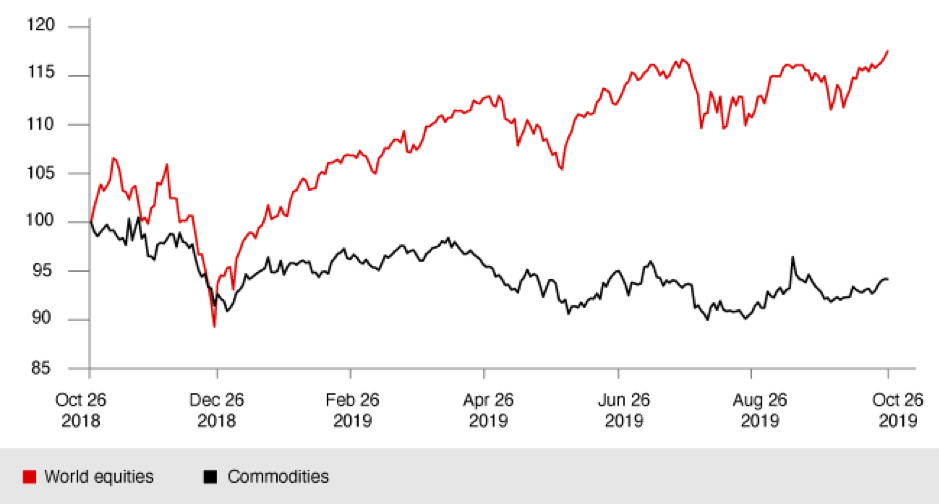

Commodities

Commodity performance over past year against equities

29/10/2018 – 29/10/2019, US dollars

Commodity prices generally have been weak, suppressed by a weaker outlook for global growth and concerns over trade. This may present marginal buying opportunities

We do not believe that we are in a bull market for commodities for a variety of reasons – weaker demand due to lower (and less commodity intensive) longer term growth expectations for China, increased commodity supply and less interest in safe haven investing (affecting precious metals). However, we retain a modest overweight exposure for the diversification benefit and because price levels do not look challenging.

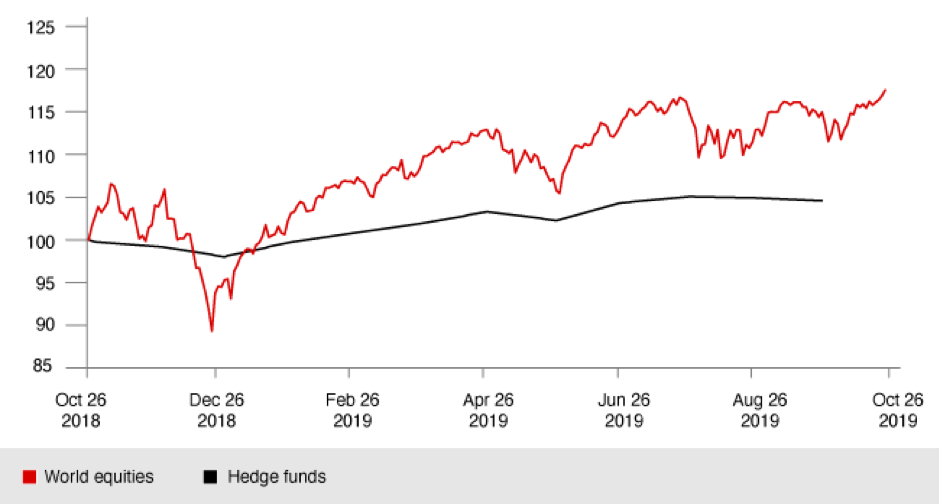

Hedge Funds

Hedge fund performance over past year against equities

29/10/2018 – 29/10/2019, US dollars, hedge funds monthly priced

Absolute performance has been disappointing through the past couple of years and fees remain high, but the diversifying qualities of hedge funds and their ability to generate alpha are more apparent with current levels of market volatility. Higher interest rates may also give hedge funds better opportunities.

Currency Funds

Sharp movements in currencies over the past year have given some opportunities for gains (and losses). These funds continue to be a useful diversifier.

Global Tactical Asset Allocation Funds

These funds can provide good diversification benefits because of their broader investment universe. However, we have been disappointed with the absolute performance from the asset class over the past number of years. We continue to closely monitor the universe of products available but remain cautious as to the ability of the asset class to produce the level of returns required over the long run. With equities at current levels, however, we believe now is not the time for clients to reduce holdings in this space.

Senior Loans

These are floating rate sub-investment grade instruments with a strong covenant and a term of between six and nine years. The premium return over cash rewards illiquidity and credit risks. The class offers another source of diversification.

Cash

Short-term interest rates remain low and sit either negative or barely positive throughout the eurozone. The ECB is under pressure to reduce rates as economic prospects weaken.

We continue to advise clients to include yield-enhancing alternatives to cash in their portfolios when this can be done at an acceptable risk.

Portfolio Structure & Risk Management

- It is very important that clients have a disciplined management framework for determining how to structure portfolios and how to adjust that dynamically over time.

- Acuvest recommends that portfolios comprise a diversified mix of asset types which balances the desire for high returns with management of the associated risks. For this purpose, we group assets into three categories: growth (including equities and property), managed risk (including global tactical asset allocation funds, certain types of hedge funds and sub-investment-grade credit risk) and defensive (including bonds and cash).

- Within clients’ portfolios, we currently advocate an overweight position in GTAA funds, short duration sub-investment grade credit, commodities and property. Balancing this, we are underweight equities.

- In a low-return environment, keeping fees low is particularly important.

- In building a portfolio, getting exposure to the equity risk premium efficiently is key. Given its low cost and avoidance of manager risk, passive investing should be considered as a baseline against which to assess the best way to gain exposure. Acuvest does, however, recommend using active managers where we believe they can add value, for example by exploiting their skill or where markets are less efficient.